[ad_1]

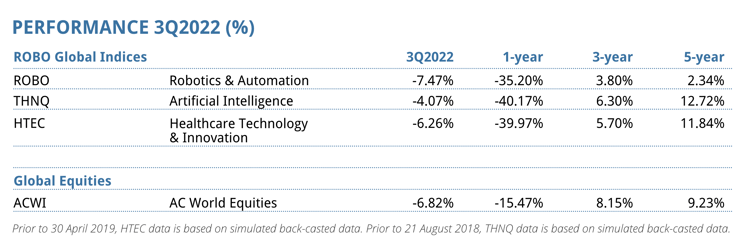

The ROBO World indices declined consistent with world equities in Q3 within the face of excessive inflation and jumbo price hikes to finish the quarter 42%-50% under their all-time highs in 2021. The Robotics & Automation Index (ticker: ROBO) misplaced 7%, the Synthetic Intelligence Index (ticker: THNQ) dropped 4%, and the Healthcare Expertise & Innovation Index (ticker: HTEC) declined 6%. Valuations have compressed effectively under long-term historic averages. On this report, we focus on main tendencies and massive movers throughout our portfolios.

Webinar Transcript:

Jeremie Capron:

Hi there everybody and welcome to ROBO World’s October 2022 investor name. My identify is Jeremie Capron, I am the director of analysis and I am speaking to you from New York. And with me at present my colleagues Invoice Studebaker and Zeno Mercer. We are going to begin with a quick reminder of what we do at ROBO World after which we’ll share some ideas about what’s taking place within the markets. After which we’ll take a more in-depth take a look at every of the three index portfolios, ROBO, THNQ and HTEC. And naturally we’ll be taking your questions, so be at liberty to sort them into the Q and A field on the backside of your display.

So let me begin with this fast overview of ROBO World. We’re analysis and funding advisory firm that is targeted on robotics, AI and healthcare applied sciences. And we handle three major index portfolios which can be tracked by almost $3 billion in belongings. These are primarily in ETFs. And our first index portfolio is ROBO, that was the primary robotics and automation index and it began nearly 9 years in the past in 2013. And the second is THNQ, T-H-N-Q, that’s the synthetic intelligence index. And the third one is HTEC, the healthcare know-how and innovation index. And you may see right here the annualized returns since inception of every index as of the top of September, 2022.

So these portfolios, they mix analysis with the advantages of index investing within the ETF wrapper. They’re composed of greatest at school corporations from all around the globe. The small, mid and enormous caps that we analysis and we rating on numerous metrics, and the best scoring shares make it into the portfolios. Then we rebalance each quarter and the result’s portfolios which have a really low overlap with broad fairness indices like DSNP 500 or the NASDAQ and different world fairness indices.

Okay, so let’s speak about what we’re seeing within the markets. And the elephant within the room right here is that the world’s greatest corporations on the forefront of robotics, of AI, of healthcare know-how as represented by the ROBO world indices, they’re now buying and selling 40 to 50% under their 2021 highs. Sure, a number of shares are on sale proper now. World equities are down greater than 25% this yr, however these usually are not your common shares right here. Once more, we’re speaking in regards to the know-how and market leaders. They’re corporations which can be usually very worthwhile and rising a lot sooner than the economic system. In truth, once we take a look at their steadiness sheets, we discover {that a} majority of the businesses within the ROBO, the AI and the healthcare tech index, they’ve more money than debt. And they also have a optimistic web money place.

And extra importantly, many of those corporations are relative beneficiaries of the present setting. When you consider the issues that we face at present within the world economic system, we now have the labor shortages, we now have rising prices throughout the board. The one clear and simple response from enterprise leaders is automation and enterprise leaders and firms are making it a high precedence. In truth, and Invoice will come again to that shortly, demand for automation at present is at document highs and rising and there’s extra demand for robots and automation that suppliers can provide.

And on the identical time, this down market in equities, we imagine is giving traders a chance to spend money on these corporations at a reduction. In truth, the three portfolios are actually buying and selling considerably under historic common valuations and we’ll come again to that. So let’s take a look at robotics and automation first, and for that I am going to move it on to Invoice Studebaker.

Invoice Studebaker:

Good morning everybody. Thanks for the time and curiosity. Jeremie, thanks for the introduction. Simply to observe up on Jeremie’s feedback, we actually know that the third quarter was a troublesome interval for traders. And September was a strong illustration of simply how troublesome it may be to be targeted on the long run horizons, significantly when the market is continually being tripped up by a confluence of points and occasions. And we perceive that these are difficult occasions. Concurrently Jeremie commented, the down market is giving traders actually a welcome alternative to benefit from deep reductions and spend money on corporations that we see they’re delivering on the mandatory automation applied sciences.

And we imagine, as Jeremie additionally commented, that this has created an setting, it is type of an ideal storm for traders, to extend publicity to a supercycle for automation and demand for automation applied sciences, as I am going to remark shortly in additional element, has by no means been greater and the problems which can be reducing fairness costs that we’re all considerably acquainted with, the labor shortages, the compressed margins, the availability chain bottlenecks and the necessity to cut back working prices are considerably rising the necessity for adoption. And as we doubtlessly go right into a recessionary setting, we predict companies are going to be very eager to wish to spend on effectivity and automation.

As you possibly can see for the quarter, the ROBO index declined about 7%, which is an identical decline for world equities, which has resulted in valuations which have compressed effectively under our historic averages. And the broad weak spot was represented in 10 of our 11 sub sectors that we invested that had proven losses. And importantly although, as we glance into the fourth quarter past, we see an ideal alternative for traders to sharpen their pencil and add to this, what we imagine, is inevitable automation theme. That is on sale like a lot of the market.

And we see an enormous discrepancy as the place inventory costs are, inventory costs are 40, 50% off their all time highs regardless of the sturdy fundamentals of automation that we’ll contact on shortly. And lots of of our constituents actually are firing on all cylinders and might’t make sufficient to fulfill the demand. As you possibly can see right here on the valuations, the PE is 12% cheaper than our historic common. And I do wish to underscore that our valuation is predicated on PE, many different tech exposures are based mostly on worth of gross sales, and in lots of circumstances are arguably over owned and overvalued. I do wish to make the remark that lower than 3% of ROBO is within the S&P 500. So it is a distinctive publicity that also could be very underneath owned and underappreciated by a lot of the market and we predict that is a chance.

Subsequent slide please. So from an EV to gross sales standpoint, you possibly can see that we’re buying and selling fairly near parity to historic valuations. So ROBO is buying and selling round 2.7 occasions EV to gross sales. Once more, the context of the place know-how trades, I imply, Adobe simply made a purchase order of an AI asset for 40 occasions trailing EV to gross sales. In order that hopefully provides you some context that I might not say that we’re hardly overvalued. Specifically, I feel our valuation of our portfolio has advanced fairly considerably through the years and has grow to be a lot growthier, in order that’s type of skewed the valuation of the upside. So I might argue that even at 2.7 occasions relative to the previous, our valuation is fairly low cost.

And simply as a construct on to that, what we have seen right here available in the market, we have had three consecutive quarter declines within the ROBO index and that is actually type of an unprecedented growth since we launched the index again in 2013. And it is solely corresponding to the again check going again to ’08, ’09. And importantly although, earnings estimates, I do know that that is perhaps type of the elephant within the room, that individuals suppose the earnings estimates are going to come back down dramatically. We actually haven’t seen that but. For 2022 and 2023, earnings estimates have solely been lower by about one to three% of the final three months and simply 6% over the past yr. And this I feel is a mirrored image of the power and demand for automation applied sciences and options.

And actually importantly, the power for ROBO corporations to deal with rising prices and provide chain challenges. Many of those corporations have been round for a few years and have had the ability set to adapt to and handle completely different financial environments and to have the ability to move on and costs. And I feel importantly, the income estimates have seen really optimistic upgrades over the past three and 12 months and level to a couple of 12% gross sales progress for 2022 and about 9% for 2023. Though the market is skeptical that estimates will not come underneath extra strain, that up to now has been the report card.

Subsequent slide please. In order Jeremy type of alluded to, ROBO is designed to be diversified, it is designed to be invested in one of the best of breed know-how corporations globally throughout the ecosystem of the know-how. So what makes the robotic or automation work? After which the functions, the place is automation being deployed? Sadly, this drawdown, as everyone knows, has been considerably violent and excessive and has resulted in probably the most vital drawdown we have seen. Even if 50% of the portfolio has what we see as an actual worth, that being uncovered to industrial automation, logistics automation, healthcare. To not point out, as Jeremie alluded to, that roughly round 60% of portfolio has a web money place and no debt. So these corporations are effectively positioned to climate the storm, like they did throughout Covid.

And this business is importantly traditionally grown the highest line two to a few occasions that of the market and we anticipate that to proceed. To not point out yr thus far, FX has been about an 800 foundation level headwind and the transfer within the greenback actually has been considerably parabolic and we predict there’s prone to be a reversion of imply and there may very well be a good tailwind as we start to maneuver into 2023 and past.

By way of the large inventory strikes, we have had a pair fortunes to the upside, not sufficient in fact, iRobot was up 57% within the quarter, as a lot of you might be conscious, they’re a frontrunner in shopper robotics and so they agreed to be acquired by Amazon in an all money transaction for 1.7 billion. This does importantly signify the twenty eighth takeout since we launched ROBO again in 2013. And whereas we will not forecast what the MA setting’s going to seem like, a lot of our corporations are, once more, leaders of their business. And as asset costs come down, we predict that they actually grow to be extra favorable within the eyes of strategic and monetary consumers.

Luminar Expertise additionally had an honest transfer to the upside. They’re a frontrunner in lidar know-how for automobiles and vehicles. The inventory was, I feel the efficiency was considerably supported by the conviction of insiders. The CEO did buy upwards of $6 million within the quarter. However importantly what’s actually transferring the inventory is their business success with bulletins. They introduced partnerships with Mercedes and Nissan, which intend to combine their know-how in most of their automobiles by 2023, or I am sorry, 2030. So we do anticipate to see extra progress right here on the business entrance.

Then when it comes to the sectors that we actually stay extremely convicted on, one space to focus on is industrial automation. And an earlier touch upon that Jeremie additionally did is that industrial automation actually is firing on all cylinders to fulfill demand. And Yaskawa, which is a big industrial robotic producer, simply introduced lately that their orders had been up 34% yr over yr. Fanuc, which is the most important industrial robotic producer, has been fairly vocal about their backlog, which now could be in extra of 1 yr. Importantly, Teradyne, which additionally performs a key position in industrial automation, has final quarter talked about their industrial automation progress was up 29% yr over yr. We anticipate that to proceed once they announce their outcomes quickly. They’re one of many largest producers of collaborative robots by way of their buy of Common Robots, which is a Dutch firm. That enterprise has additionally actually been firing on all cylinders. That enterprise final quarter noticed robotic gross sales really up 30% on a 55% comp.

So enterprise actually stays fairly robust and wholesome. These asset costs are actually fairly attention-grabbing for traders to try. And general, in the event you take a look at robotic density, and in order that’s trying on the variety of robotic installations per 100 individuals, imagine it or not, the worldwide common is only one.2 robots per 100 workers. And so we now have an extended approach to go when it comes to the place penetration charges are going. Simply to place that in context, the US has roughly 2.5 robots per 100 workers. China can also be 2.5, however they’ve grown from 0.5 to 2.5 in 5 years. So fairly superb progress there. Japan’s about 4, Germany’s 4 and Korea is 9.

So this all is within the context of a world setting the place world manufacturing employs about 500 million individuals globally. So if robots are stealing our jobs, they don’t seem to be doing an excellent job of it and we predict there’s vital progress within the years forward. That is it for my ready marks. I suppose I am going to move it on to-

Moderator:

Thanks Invoice. Hey Invoice, earlier than we transfer on, we now have a particular query to ROBO from the viewers round why we embrace Nvidia however not Micron or Intel or STM. May you communicate to that?

Zeno Mercer:

Positive. Hello. Hey everybody. Zeno right here masking THNQ at present. And okay, might you repeat that query? It was round possession?

Moderator:

Sure. So that they’re asking within the ROBO Index, we embrace Nvidia however not Micron or Intel or STM. So might you discuss in regards to the distinction between ROBO and THNQ and the place these corporations would fall?

Zeno Mercer:

Proper, okay. I feel the best way we take a look at it isn’t solely, sure, these are all concerned in elements of type of fashionable society, robotics, AI, however we’re on the lookout for corporations which have maybe probably the most funding or publicity to those areas. And I am really going to cowl in a video later, however I might say some issues now, at their latest AI day, they’re closely invested not solely within the chips however the software program aspect of issues. And at that time we take into account them extra of an AI and robotics play. I imply, they’ve software program particularly for it and we simply have stronger conviction round it going ahead. Clearly corporations like Micron are making huge investments and are essential to society, however we’re attempting to get publicity to particular areas and never simply make investments normally corporations within the area. I imply, we are able to cowl extra later once I discuss extra about Nvidia for a bit.

Yeah, we are able to go to the following slide. Reflecting on the quarter, the THNQ index was down 4%, really outperforming world indices and the S&P, and we’re down 47% since November 2021 excessive. So the AI area has been underperforming even whereas fundamentals have been bettering in some ways. And I am going to get to that. From a valuation standpoint, Ford EV gross sales are persevering with downward and so they’re really on the quarter finish, they’re at 4.6, which is under March 2020 lows. Even whereas adoption progress, digitization and plenty of huge tendencies and tailwinds are coming, not solely now however 2023 and past. And we’ll cowl that. And a few of the huge issues that occurred is we had earnings deceleration this yr all the way down to 11.2%. So general our corporations grew, however this was down from 27.9% in 2021. Clearly it was a really huge yr for income.

And the present forecast proper now could be a stronger rebound again within the low twenties for 2023, 2024. So proper now, I imply, this has been a troublesome yr. Folks have been type of reorganizing and determining what strikes they’ll make, however sure areas of the economic system are seeing and have huge backing for continued funding over the following a number of years and quarters. So I feel it is essential to suppose and know that AI is changing into an rising share of company authorities spend and it is also an enabler of GDP progress and value financial savings. So there’s each progress elements and deflationary elements which can be concerned right here and we’ll cowl that.

Subsequent slide. Yeah, so we really had, regardless of the index being down, we had outperformance, we had 79% beat high line expectations and 85% beat earnings. And I feel round 87% are anticipated to be worthwhile subsequent yr. So in the event you’re enthusiastic about these corporations, we now have excessive pricing energy, they’re essential gamers to the economic system, whether or not it is funding spend from the Fortune 500 seeking to digitize their merchandise or make new merchandise and even simply discover price financial savings throughout provide chain, operations, issues like that. And even simply utilizing AI as a core product and to extend the product growth, whether or not actual world world merchandise or digital merchandise, options. So there’s developer operations, cybersecurity, plenty of angles there.

Many corporations even have raised steerage within the index resembling Samsara, which really raised 3 times this yr regardless of their very own provide chain issues. That is high line and backside line. From huge knowledge and analytics, we really noticed a standout from corporations like Alter X, which is seeing 50% yr over yr progress and 90% gross margins. And regardless of everybody being afraid of, oh, what is going on to occur with spend, and the place cash goes is shifting this yr, I feel we’re all seeing that. And Alter X is seeing their largest pipeline in historical past for digitization automation of bringing in knowledge and determining what to do with it and discovering methods to streamline capabilities with elevated labor price, inflation.

So these corporations present very excessive ROI and that is why once we’re setting up and reevaluating the index and rebalances, we’re taking a look at what corporations are enablers proper now. And that is each the infrastructure aspect and the precise software aspect which can be really getting used at present. It is the availability and demand. And also you would not construct semi chips, there is not a cause, and I am going to get to this subsequent, in regards to the CHIPS Act, if there weren’t an essential aspect coming down the road for that. And most of these chips, the chips being produced there aren’t going to be coming on-line till 2025 and past.

So we are able to really go to the following slide now. I suppose I already lined the outperformance right here, nevertheless it was, regardless of points within the economic system, it was a really robust quarter and we noticed fairly strong reassuring steerage from many areas. I feel one of the vital troubled areas is on shopper, though our shopper index or the patron sub sector and e-commerce had been one of the best performing this final quarter, they’d oversold in Q2.

So in the event you’re type of on the lookout for 1 / 4, I imply you are going to have shifts there, however that is why we even have publicity and make allocations of those completely different areas. Going to speak about Semi actual fast, I feel one of many largest issues that occurred was two issues. A, we handed the CHIPS Act and we additionally had US commerce restrictions, Semi efficiency regardless of the CHIPS Act being handed, regardless of Europe additionally declaring they wish to double manufacturing of Semi chip capability themselves, getting away from Asia manufacturing area, our Semi index was down 12%.

A part of it’s falling in lockstep with the economic system and the whole lot else. A part of it’s type of overblown fears round what’s taking place with the China commerce restrictions and likewise round shopper, PCs, Cell. Apple introduced that they’ll not enhance manufacturing of the iPhone 14. And we now have some publicity there, however general that is PC and private. When you’re speaking about cloud, AI, automotive and connectivity, which is the place we really attempt to allocate extra publicity to on that aspect of issues, on the infrastructure aspect, we’re really seeing robust demand and forecast. For example, Qualcomm, which is concerned in lots of, they’ve I feel $7 billion enterprise models. They’ve seen their automotive pipeline go from 19 billion to 40 billion in a single quarter. So the inflation discount act, all these items persons are making, we do not have full EVs but, no less than within the sense that they don’t seem to be in all places.

I imply, in the event you take a look at share of automobiles on the highway, it is 0%, 0.001. Nonetheless, clever sensible automobiles that require extra processing, you have bought EVs, they require extra semiconductor chips and processing connectivity and also you’re seeing a giant increase in demand spike there. So whereas we’re seeing a oversaturation in that section, we’re seeing huge progress. After which there shall be one other improve cycle for wearables and issues like that, that that’ll come again on-line. However it’s type of smoothing out the method right here. And that additionally includes elements, sensors and laptop imaginative and prescient.

By way of cloud demand, we’re seeing huge pull by way of nonetheless. Arista, which makes networking switches and software program for these huge cloud middle deployments from the large tech corporations and enterprise and others. They supplied very strong steerage in 2023 at their final name. So in the event you’re trying by way of the noise and seeing what’s an indicator of issues to come back, it is continued funding on this area. And we have got a number of hundred billion greenback plus tailwinds coming by way of 2023 and past. And it could not be extra apparent how essential it’s than if you get to the commerce restrictions.

However the CHIPS Act, simply to present everybody an instance of how we take a look at the infrastructure area, they need to make the semiconductors themselves, so you will have Nvidia, Intel, Samsung, gamers like that. You even have corporations like LAMB Analysis and ASML, which make crucial elements to that. To make tiny three nanometer elements, you want very costly, very refined gear. I imply, it is a few of the most spectacular tech we now have on the planet proper now. Every of those gadgets although have a few years pre-order, there is a backlog, and so they run $180 million per pop for ASML for instance, it is a Dutch based mostly firm.

As a share of spend, okay, for instance there is a $50 billion Chips Act and a whole bunch of billions coming on-line in manufacturing within the US for instance, not even speaking in regards to the EU, one $17 billion plant in Texas, $10 billion of that’s going to semi manufacturing gear. So simply to present you a scale, and I do not suppose the market’s actually reflecting that, semi’s useless, lengthy reside semi, persons are like, “Oh, PC, gaming,” there’s a lot approaching board. I feel that is one thing to remember if you’re sitting right here enthusiastic about what’s snug and what’s really going to get cash within the subsequent couple of years.

China restrictions, Nvidia, Nvidia’s had a tough yr, gaming’s down after which the China commerce restrictions have come on board. They don’t seem to be set to start out for some time till subsequent yr, 3Q subsequent yr. And it really leaves them with some wiggle room. So it is not essentially they can not promote into China, they only cannot promote particular chips and issues. Truly rumors are saying that they are really getting a number of orders and persons are stockpiling proper now. So take that as you’ll. However I feel in the end it simply reveals how essential these are and that there is going to be elevated emphasis and funding right here.

One other factor I needed to speak about briefly is the Tesla robotic. That was a fairly large deal for a lot of, within the sense that it introduced consideration to the area. Elon has that impact. He targeted on EVs, he mainly made the EV market. Robots although are already a giant market, clearly that is why you guys are all right here is attempting to grasp and listen to that and from our angle. So what I feel goes to occur right here is A, shopper robots have very low penetration. In truth, it is mainly null. You do have extra automation in semi and automative and manufacturing, nevertheless it’s one other market that actually is not being appreciated is the robotic area and AI area with the ability to visualize and mainly, they need to function within the digital world to have the ability to function within the bodily world. That is going to take elevated computation and funding in cloud, AI, connectivity.

So I feel that is the takeaway there. I do not actually wish to make a projection on when will Tesla robotic be in individuals’s properties if it should, et cetera. However I feel it is simply one thing to remember.

Yeah. So talking of recent issues, we have got a brand new addition. We added CrowdStrike this quarter. So CrowdStrike for many who do not know, is an American cybersecurity firm that was based in 2011. That they had their first product in 2013. They have been on a roll right here. We have been watching them for a while and so they’ve actually confirmed resilient. And once we’re enthusiastic about making an addition to an index, we take a look at quite a lot of issues, We take a look at their market and know-how management and we additionally take a look at what are they investing in, have they got a pipeline of merchandise which can be going to proceed to make them achieve market share and increase their addressable market.

Proper now they have been rising, their 5 yr progress price is 94% anticipated to hit 1.5 billion this yr and a couple of.2 billion subsequent yr. So their AI enabled cybersecurity options are trusted worldwide, with a TAM addressed estimated to be $75 billion and that is rising to 125 billion with new merchandise. They’ve a 97% retention price and so they turned worthwhile in 2021. So this is not just a few progress story. Their EPS is projected to develop 50% over the following a number of years. Going again to funding, they’ve 25% of their income investing within the R&D and in merges and acquisitions. They’re making sensible acquisitions, they’re investing, we’re very assured that they’ll proceed to be a frontrunner in AI enabled cybersecurity.

At this level, I am going to move it on to Jeremie to debate our healthcare index.

Jeremie Capron:

Okay, thanks Zeno. So HTEC is the healthcare know-how innovation index that we launched in 2019. And in the previous couple of years we have seen the convergence of robotics, AI and life sciences that has enabled some breakthrough advances. And we imagine that healthcare is the one huge financial sector that is going to be profoundly remodeled by know-how over the approaching decade. And so we construct the HTEC index utilizing an identical recipe to the ROBO index. Meaning the index portfolio consists of one of the best at school corporations from around the globe which can be reworking the healthcare business throughout 90 areas you could see on this pie chart. So there’s robotics, which is about robots within the working room, within the pharmacy, in hospitals and so forth.

And you’ve got knowledge analytics, which is about corporations utilizing software program to derive insights from the information that we now gather round sufferers. The information from medical trials, the information from medical imagery and AI is more and more utilized in diagnostics and drug analysis and automating, or it is extra about augmenting the work of clinicians, augmenting the pace and accuracy of a diagnostic. After which you will have telehealth, which is about decentralized medication, like distant physician affected person visits that we’re now all acquainted with, nevertheless it’s additionally about wearable gadgets for the monitoring of glucose ranges or cardiac exercise and so forth.

You’ve genomics in fact with corporations offering the instruments to decode the genome and corporations creating early most cancers detection options. You’ve corporations with gene enhancing know-how and even artificial biology the place we create artificial genes. After which lastly you will have a bunch of medical and surgical devices like 3D printed implants, you will have coronary heart pumps, miniature coronary heart pumps, neurovascular instruments and so forth. So it is a fairly numerous basket of presently 78 corporations, huge and small.

In truth, almost half of the businesses within the portfolio are small and mid caps, however they’ve one factor in frequent, which is know-how and market management of their respective sectors. And on the following slide you possibly can see that the portfolio carried out very effectively in 2019, 2020 and 2021 earlier than that type of indiscriminate promoting basically lower in half. And so the HTEC index has now declined 50% from its excessive of February 2021. And within the meantime, the income has grown by greater than 30%. So income grew by 22% final yr. And this yr we’re going to see a further 12% and subsequent yr we’re taking a look at 10% gross sales progress, 2023. So HTEC is now buying and selling on 3.9 occasions ahead enterprise worth to gross sales. That is on the median for the basket. And that compares to the excessive yr of seven.2 occasions and the low within the Covid lockdown panic, that was 4 occasions. So we are actually under the Covid lows when it comes to valuations and I feel that is a very essential level to remember.

So I wish to contact on a few of the corporations right here so that you get a greater sense of what is within the portfolio. And I’ll begin with a few of the high performers throughout the quarter. You possibly can see Butterfly Community’s right here, that was up over 50% prior to now three months. So Butterfly’s in our diagnostic sector and it has developed the IQ ultrasound resolution, that is an ultrasound system that’s 80% cheaper than conventional gadgets. It is small, it really works with smartphones and tablets and has a software program platform that’s subscription based mostly. So that they’re increasing entry to ultrasound based mostly analysis dramatically. And it is rising very quick, about 30% per yr, with margins above 50% on the gross stage. So Butterfly has $300 million within the financial institution, so loads of room to proceed to scale and in the end we predict it is a very probably acquisition goal.

After which Penumbra right here, Penumbra is an organization in our medical machine sector. They’ve developed very revolutionary surgical devices for neuro and vascular situations. So it is about stroke therapy and eradicating clots and thrombectomy and coiling techniques. And Penumbra’s tech is superior to the normal stent strategy, in order that they’re additionally rising quick, like 15, 20% a yr. And so they have higher than anticipated margins once they reported and so they’re speaking about accelerating progress and procedures into the rest of the yr. They’re making aggressive positive aspects. Additionally they have quite a few merchandise developing over the following 18 months.

And AxoGen, you possibly can see right here, which was up greater than 40%, that is in a regenerative medication sector. AxoGen has developed an answer to restore the bodily injury to nerves, peripheral nerves. And they also’re capable of restore feeling and performance of nerves. Principally it is a nerve graft and it is the one off the shelf human nerve allograph in the marketplace. And AxoGen additionally had higher than anticipated income final quarter. And the administration commented that they anticipate the gross sales progress to return to mid teenagers by the top of the yr.

And eventually, I needed to the touch a bit bit on genomics and precision medication, which collectively account for a couple of quarter of the portfolio. And you may see on this slide some examples of corporations in HTEC, a few of the know-how and market leaders which can be actually powering the genomics business. And we predict genomics is totally a revolution and it is taking place now. It is a revolution as a result of genomics allows a very new strategy to medication and the early detection of illness. It isn’t solely hereditary illness but additionally persistent illness like most cancers. And since it additionally allows customized remedy, customized remedy which means individualized remedy versus the present mannequin of huge pharma the place you will have a one dimension suits all type of molecule that price billions of {dollars} to deliver to market. Right here we’re speaking about therapies which can be tailor-made to the person.

And the rationale why this revolution is occurring now could be as a result of we now have reasonably priced gene sequencing know-how and the price of sequencing the human genome is declined dramatically from billions of {dollars} with the primary human genome undertaking a long time in the past to now underneath $1000. And if there’s one firm that is been main the cost when it comes to driving down the price of gene sequencing, that’s Illumina, which is the market chief. They’ve greater than 20,000 machines put in worldwide. They’ve greater than 75% market share globally. And final yr they grew income by 40%. And about two weeks in the past they launched the brand new NovaSeq X, which is the brand new sequencing platform that would take sequencing prices down by greater than half to only a few hundred {dollars}. And the final time we noticed such a big price decline, that drove fivefold enhance available in the market dimension for genomic sequencing.

And that is what allows genomics testing. And I discussed the early detection of the ailments like most cancers. So Natera for instance, is the market chief in prenatal DNA testing. They’ve a non-invasive check for abnormalities and Natera is now pushing into most cancers screening and implant rejection testing as effectively. Veracyte, that is one other firm that is reworking the diagnostic of most cancers utilizing DNA know-how. They’re working in thyroid and lungs and breast most cancers testing. They’re rising the accuracy of diagnostic and avoiding pointless surgical procedures for sufferers.

And I additionally spotlight Twist Bioscience right here. Twist is the chief in DNA writing. So it is the synthesis of genes which they do with a silicon chip to fabricate big selection of artificial DNA at a low price. They now have 1000’s of consumers together with pharma corporations, together with analysis facilities, but additionally industrial corporations, chemical corporations, agricultural corporations.

And eventually I wish to contact on Alnylam. Alnylam is an effective instance of precision medication and individualized remedy. They pioneered the RNA interference therapeutics, we name that RNAI. And so they simply obtained their fifth approval in lower than 4 years for the therapy of polyneuropathy illness known as ATTR. And this therapy that they are developing with might attain billions of {dollars} in gross sales. So if you examine that to the market cap of Alnylam at present, there’s I feel attention-grabbing discrepancy.

So in whole there are 18 corporations in our genomics and precision medication section and so they account for round 25% of the HTEC portfolio. And I hope you perceive that there our portfolio building course of right here is admittedly about diversification, offering publicity not solely to small areas like genomics, precision medication, however to all areas of the healthcare business the place know-how is making a distinction.

All proper, so I’ll pause right here. I feel we have lined a number of floor, I actually wish to take a few of your questions and I see we now have a query about earnings trajectory for our portfolios. What’s the anticipated earnings progress for this yr and subsequent? And I feel we are able to begin with ROBO. I am going to touch upon ROBO after which Invoice and Zeno can touch upon the opposite portfolios. However basically we predict we’ll shut 2022 with about 15% EPS progress for ROBO. So final yr we had greater than 40% EPS progress. This yr we’re nonetheless taking a look at 15, which is considerably forward of what you’d anticipate for the S&P 500, significantly in the event you exclude the power sector from the S&P 500. We’re mainly taking a look at a compression in EPS for this yr for the broad market. For ROBO, it is 15%. And for subsequent yr, we’re taking a look at about the identical, so 15 to 17% is the anticipated EPS for ROBO in mixture for subsequent yr. Zeno, do you wish to touch upon AI?

Zeno Mercer:

Sure, Hello. Yeah, so when it comes to EPS progress for the THNQ index and its members, I am going to type of break up it into software and companies and the infrastructure part. Infrastructure has been a bit smoother this yr and we noticed 29% EPS progress in 2021, this yr we have seen and projecting for the total yr, 22%. So a slight pull down. On the flip aspect on software and companies, we noticed 29% final yr and seven.9% this yr, with eCommerce and shopper being the largest laggards. However that is anticipated to rebound within the following yr respectively, shopper and e-commerce to 25% and 64%.

And I feel trying 2023 and past, the projections are taking a look at 11.6 this yr. General THNQ index is seeking to get again into the twenties progress for EPS, so 20.4 after which even greater clip in 2024 and past. I feel a few of the standouts inside that may be community and safety, which is rising at 49% this yr and anticipated to nonetheless keep higher twenties, low thirties subsequent yr. So that you’re seeing some rebound in some areas and others are simply going to see continued power for EPS.

Invoice Studebaker:

Jeremie, simply to fall on to your feedback, perhaps nearly revenues for ROBO, I feel importantly, that is type of the elephant within the room, everybody thinks there’s going to be a fairly dramatic discount in estimates. Clearly we have not seen that occur. That could be a threat. Income progress ROBO is actually anticipated to be about 13% this yr and subsequent yr a bit over 8%, which is consistent with its historic averages. So even when there’s strain from the broader markets, we do anticipate our indices to usually develop two to a few occasions to that of the market, which traditionally they’ve. So we really feel fairly good about the place these companies are positioned as we go into 2023 and past.

Jeremie Capron:

Okay, thanks Invoice and Zeno. And I see we now have a query about potential ESG points with the genome oriented corporations, particularly governance considerations. So right here at ROBO World, we take ESG very severely. We launched our ESG coverage in 2017, so happening 5 years now. And we have improved the coverage persistently through the years, primarily given the pool that we had from a few of our European traders. And so the coverage at present is extraordinarily full and yow will discover all the main points on the web site and it is actually targeted on excluding corporations that fail sure requirements that we have established consistent with the Febelfin requirements over in Europe. It is one of many strictest requirements. So we take a look at environmental efficiency, governance and social points in fact. We use our personal inside analysis to guage each firm that is in our funding universe, however we additionally use exterior assist from maintain analytics that helps us flag any potential points or controversies as they come up.

Now when it comes to query across the genome, I feel it is an space the place we’re seeing a number of debate, whereas isn’t any debate is round utilizing genomics for early detection of illness as a result of the idea right here is that you’ll be able to choose up a illness earlier than it turns into an infinite downside when it comes to your capacity to treatment, in fact, and your chance of survival, but additionally when it comes to the price to the healthcare system. And so there appear to be unanimous view throughout the business and coverage makers round the truth that genomics in diagnostics is a no brainer. And so we do not anticipate any points there. The place some points might doubtlessly come up I feel is round gene enhancing as a result of right here we’re making adjustments into the human DNA. In lots of circumstances we’re making adjustments into cells in order that it may possibly produce particular proteins and proteins that can assist battle towards a illness.

And it’s nonetheless very early days. In the present day there isn’t any FDA accepted gene enhancing based mostly remedy. However in 2020 we noticed the primary dosing of a human affected person with such an strategy and we had some pretty promising outcomes with that and that is why you have seen the gene enhancing shares carry out rather well in 2020 and first half of ’21. Now they’ve come down a good distance, however I feel that is the place we have to pay a bit extra consideration.

And the final remark I might make round that’s that clearly we have seen a change within the trajectory on the FDA when it comes to how briskly they have been approving gene therapies and cell therapies. So for a very long time till I would say round 2019 or so, there was reluctance by the FDA to quick monitor this analysis. However at present it has been a transparent acceleration and whereas there’s solely a handful of gene and cell therapies accepted available in the market at present, there is a backlog of a number of a whole bunch of these presently in medical trials. And so we anticipate the raft of approvals over the following a number of years.

So I’ll cease right here once more, if you wish to deliver up any questions, please sort them into the Q and A field. There is a query in regards to the autonomous system, sub sector, I feel Invoice, you would possibly wish to take that. It is presently at 0%, was considerably greater than that, Invoice, you wish to give some coloration.

Invoice Studebaker:

Yeah, that is proper, it’s 0% proper now. And we did have one constituent in there, which was iRobot, clearly taken out. And simply because an organization is faraway from an index, we do not mechanically simply put one thing in, as Jeremie talked about within the earlier a part of the presentation, we’re seeking to establish corporations that we predict are leaders of their business, corporations which have a technological mode round their enterprise, have dominant market shares. In order that’s a very essential standards for what we’re on the lookout for.

And we do anticipate the patron sector to start to evolve. Clearly we’re fairly enthusiastic about Tesla’s ambitions right here and I feel as the value factors come down, because the use circumstances broaden, I feel we’ll see a pure evolution within the shopper sector, however we have not had a number of progress there but. With regard to your query, I suppose you had been commenting about Group Gorge and one other entity in Spain. Once more, I feel the essential attribute about what we’re attempting to do at ROBO is put in leaders within the business. Whereas these corporations might have some ambitions in robotics, they’re clearly not getting there but. Group Gorge in France particularly, not solely would we query their market share in technological management, there’s a liquidity difficulty for corporations to go in our index, they need to have a minimal market cap and minimal liquidity per day. And each of these corporations would fail these screens. So I do not, Jeremie, some other ideas, however that is.

Jeremie Capron:

Invoice, there’s one other query about FX attribution for ROBO yr thus far. I do know you touched on that earlier. Do you wish to repeat that?

Invoice Studebaker:

Yeah, clearly it has been a giant headwind. It has been round 800 foundation factors since we launched yr thus far, it is most likely about 12, 1300 foundation factors since we launched in 2013. So we have really absorbed that quite effectively, we actually would hope that that may grow to be a tailwind. There have been years the place FX has been a tailwind and whereas we will not anticipate that, we actually do not hedge for it. And we predict over time there’s a reversion in imply that usually occurs in forex markets. And on condition that the best way the index is constructed, we’re attempting to establish corporations that we’re detached to the place they’re situated. It simply so occurs about 45% of our index is in North America and about 55% internationally. And once more, crucial attribute for us is defining who the market leaders are, business leaders, know-how leaders, and we’re detached to what we area they’re in.

Jeremie Capron:

Okay. We have now one final query in regards to the turnover that we see within the index. I’ll take that. So basically the turnover comes primarily from the quarterly rebalancing. The index itself is fairly secure when it comes to the constituents. Now in fact the weightings can change on the margin because the scoring evolves, so we rating each firm in our analysis universe and the rating drives a legibility into the portfolio and to some extent the place dimension.

Scores evolve every time the analysis crew interacts with the corporate or there is a company motion, there’s new details about market management or know-how management. Additionally the income publicity to the issues that we’re going after, the scores will transfer, however the major driver of turnover is admittedly the rebalance when each quarter we return to that rating pushed weighting. And in order that drives about 25 to 35% turnover in a typical yr, so 4 rebalances per yr. However the adjustments when it comes to constituents actually usually are not that significant. In truth, each quarter you will usually see one or two new inclusions or exclusions on the basket of about 80 corporations. That is the place the turnover comes from.

Zeno Mercer:

I am going to add one thing to the THNQ index actual fast. Considering by way of THNQ, we now have 71 index members and this previous quarter we had 4 takeouts, one addition. Final yr we had 5 or 6 takeouts from M&A alone. And one of many takeouts was iRobot, which was additionally within the THNQ index. There’s not that a lot overlap, however that was one, it was in AI and ROBO play. So I simply needed so as to add that we’re making strikes there. And I feel what we have thought of quite a bit currently is simply because the entire market is down, we’re trying to verify we seize the businesses which can be strong and never simply following in tandem, however we’ll make it possible for they’ll develop market share, have invested correctly, have resilient management going ahead and to the following quarter and past. So. Yeah.

Jeremie Capron:

All proper. Effectively, I feel we’re happening the hour, so I wish to thank everyone for becoming a member of us at present and remind you you could join a biweekly e-newsletter on the web site roboglobal.com, the place we share a few of our analysis and insights into corporations and sectors, robotics, AI, and healthcare know-how. And we very a lot look ahead to chatting with you once more sooner. Thanks.

[ad_2]